Executive Summary

The global landscape in 2026 is defined by a significant escalation in data privacy and cybersecurity regulation, coupled with increasingly sophisticated and costly cyber threats. The era of passive compliance has ended, replaced by a new paradigm of aggressive regulatory enforcement, particularly in the United States and Europe. Businesses face a convergence of new comprehensive state privacy laws, stringent EU-wide cybersecurity directives, and sector-specific rules that demand a higher level of operational maturity.

Key takeaways include the rising financial impact of data breaches, which cost an average of $4.44 million globally in 2025, with the U.S. reaching an all-time high of $10.22 million. AI is a dual-edged sword, driving a new wave of sophisticated attacks while also offering advanced defensive capabilities that can reduce breach costs by nearly $1.9 million. Regulators are targeting publicly visible compliance failures, such as broken opt-out mechanisms and non-compliant privacy policies, with enforcement actions resulting in multi-million dollar settlements.

Emerging trends demanding immediate attention are the heightened focus on children’s privacy, new restrictions on sensitive data like precise geolocation and neural data, and the mandating of universal opt-out signals like the Global Privacy Control (GPC). Simultaneously, the legal cannabis industry is navigating a period of profound regulatory recalibration globally, from federal rescheduling in the U.S. to market-shaping policy reversals in Germany and Thailand, creating a complex matrix of compliance, financial, and cybersecurity risks. Proactive governance, automated compliance solutions, and a deep understanding of the evolving legal frameworks are no longer strategic advantages but essential for operational survival and resilience in 2026.

Global Data Privacy and Cybersecurity Landscape

The regulatory and threat environment in 2026 is characterized by increasing complexity, heightened enforcement, and the transformative impact of new technologies. Key global trends are shaping compliance obligations and risk management strategies for organizations across all sectors.

Core Themes and Developments

- Shift to Aggressive Enforcement: 2025 marked a significant pivot by regulators from finalizing regulations to pursuing aggressive enforcement. The “wait and see” or “fix it later” approach to compliance is now largely obsolete, as cure periods are expiring in many jurisdictions and regulators are targeting publicly viewable issues like non-compliant privacy policies and confusing opt-out processes.

- Proliferation of Legislation: The number of comprehensive privacy laws continues to grow. In the U.S., 20 states now have such laws in effect as of January 1, 2026. The European Union is actively implementing a suite of landmark legislation, including NIS2, DORA, and the Cyber Resilience Act, creating a complex, multi-layered regulatory framework.

- Focus on Sensitive and Minors’ Data: There is a pronounced global focus on protecting minors and regulating the processing of sensitive data. New laws impose strict age-gating requirements, parental consent mechanisms, and advertising restrictions for children’s data. Concurrently, the definition of “sensitive data” is expanding to include categories like precise geolocation and neural data, which now require explicit consent for processing in many jurisdictions.

- Data Sovereignty and Cross-Border Transfers: Geopolitical concerns are driving a focus on data sovereignty. Canada released its Digital Sovereignty Framework, and the U.S. is enforcing regulations like the DOJ’s Data Security Program Rule and the Protecting Americans’ Data from Foreign Adversaries Act (PADFA) to impose strict requirements on transfers of sensitive data to foreign adversaries or countries of concern.

The Evolving U.S. Privacy Framework

The United States continues to develop a complex patchwork of state-level privacy laws, with 2026 marking a critical year for new legislation coming into effect and a demonstrated increase in regulatory enforcement.

New Comprehensive State Laws Effective in 2026

As of January 1, 2026, new comprehensive privacy laws have become effective in three states, expanding the U.S. baseline and requiring businesses to adapt to new consumer rights and controller obligations.

State

Law

Effective Date

Applicability Thresholds

Key Consumer Rights

Indiana

Indiana Consumer Data Protection Act (INCDPA)

Jan 1, 2026

100k consumers / 25k consumers + 50% data-sale revenue

Access, correction, deletion, portability, opt-out of targeted ads, sales, profiling

Kentucky

Kentucky Consumer Data Protection Act (KCDPA)

Jan 1, 2026

100k consumers / 25k consumers + 50% data-sale revenue

Access, correction, deletion, portability, opt-out

Rhode Island

Rhode Island Data Transparency & Privacy Protection Act (RIDTPPA)

Jan 1, 2026

35k consumers / 10k consumers + 20% data-sale revenue

Access, deletion, opt-out of targeted ads, sales, profiling

Major Amendments and Youth-Protection Laws

Several states have enacted significant amendments and new laws focused on minors’ privacy, sensitive data, and consumer rights, which take effect in 2026. These changes introduce highly specific and stringent operational requirements.

State

Law / Amendment

Effective Date

Key Changes and Operational Impact

Connecticut

CTDPA Amendments

Jul 1, 2026

Expands “sensitive data” to include neural data; strengthens minors’ protections.

Oregon

OCPA Amendments

Jan 1, 2026

Bans the sale of precise geolocation data; requires honoring universal opt-out signals; cure period ends.

Texas

App Store Accountability Act

Jan 1, 2026

Mandates age verification and parental consent for minors on app stores.

Utah

Utah Digital Choice Act

Jul 1, 2026

Requires social graph data portability and mandates interoperable protocols for social media platforms.

Virginia

VCDPA Social Media Amendments

Jan 1, 2026

Limits minors’ social media use to one hour per day absent parental consent; tightens profiling restrictions.

Arkansas

ACTOPPA

Jul 1, 2026

Imposes strict data minimization and prohibits targeted advertising to users under 16 without consent.

Nebraska

Parental Rights in Social Media Act

Jul 1, 2026

Requires verifiable parental consent for social media users under 18.

Enforcement Risks and Regulatory Trends

- Executive Liability: California now requires a member of a business’s executive team to attest to the accuracy of risk assessments for certain data processing, elevating privacy to a governance mandate with personal legal risk.

- Rising Settlement Costs: Enforcement actions are becoming more costly. California has reached multiple settlements exceeding $1 million, such as a $1.5M+ penalty against Healthline Media for failing to honor Global Privacy Control (GPC) signals and a record $1.35M penalty focused on employment-data disclosures.

- Focus on Universal Opt-Out: Regulators are prioritizing enforcement of consumer opt-out rights, with a particular focus on technical compliance with universal signals like GPC. Failure to honor GPC is now a key enforcement target.

- Targeted Issues: Regulators are cracking down on precise geolocation data processing, non-compliant data-protection-addendum language in contracts, and “dark patterns” in user interfaces, such as making it more difficult to opt out than to opt in.

- CIPA Litigation: The California Invasion of Privacy Act (CIPA) continues to fuel class-action lawsuits related to online tracking tools. A November 2025 ruling in Camplisson v. Adidas found that tracking pixels could plausibly constitute a “pen register,” signaling continued and significant litigation risk for website operators.

European Cybersecurity and Data Regulation

The European Union and the United Kingdom are in a decisive phase of implementing comprehensive and interlocking cybersecurity regulations, shifting the focus from preparation to active compliance and creating a more demanding environment for businesses operating in Europe.

Key EU Legislative Frameworks

- NIS2 Directive: This updated cybersecurity framework extends beyond critical infrastructure to sectors like digital services, manufacturing, and ICT providers. It differentiates between “essential” and “important” entities, both subject to strict cyber risk management and incident reporting. Member states are transposing it into national law, with Germany’s NIS2 law already in force. Regulators are expected to begin active supervision and audits in 2026.

- Digital Operational Resilience Act (DORA): Applying to the financial sector, DORA mandates that all ICT service contracts incorporate specific resilience clauses, a requirement that has been in effect since January 2025. This creates a dual compliance challenge for providers, who must meet DORA standards and manage their own subcontractors.

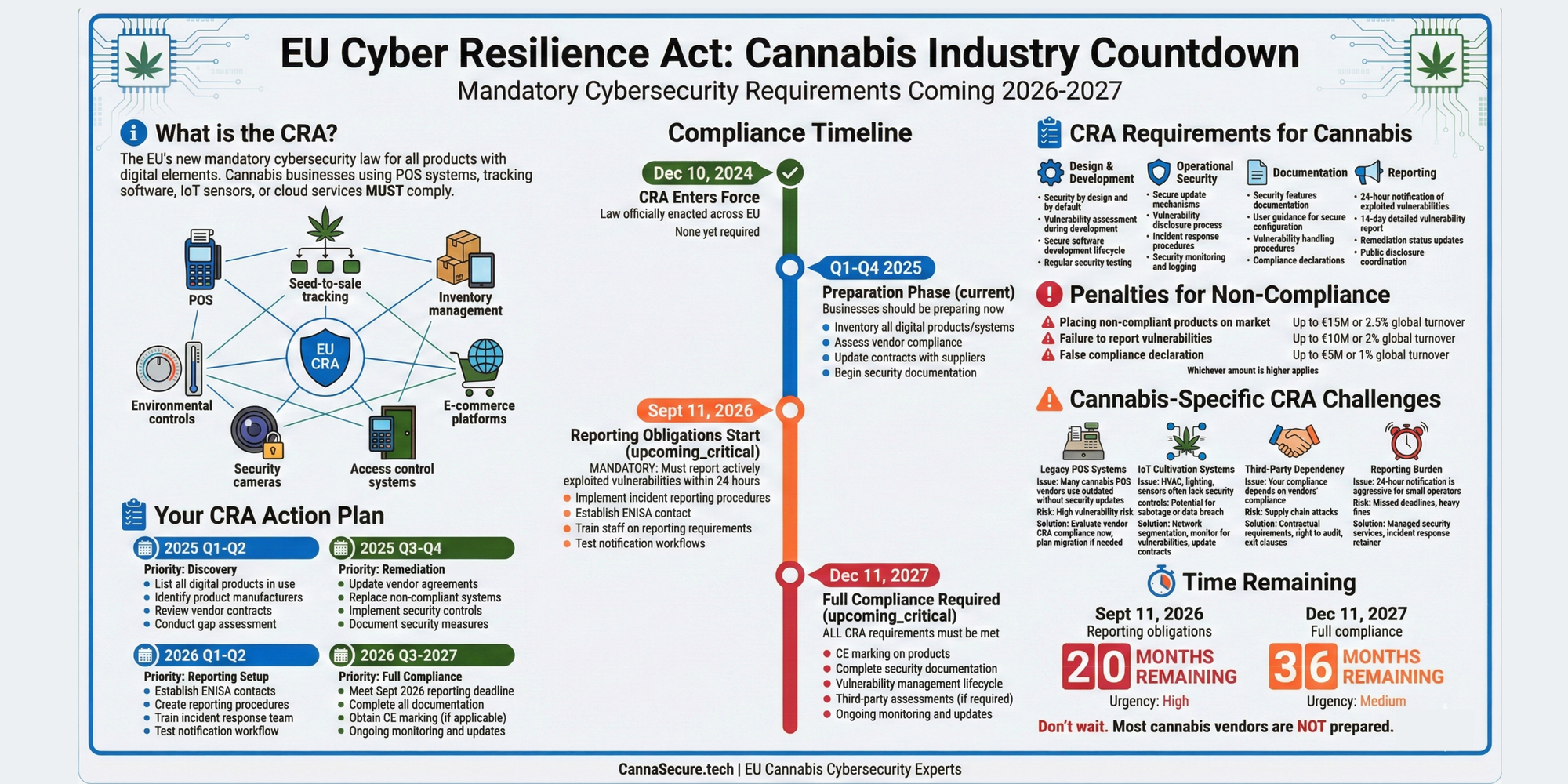

- Cyber Resilience Act (CRA): Now in its implementation phase, the CRA imposes baseline security-by-design standards on nearly all products with digital elements sold in the EU. Vulnerability and incident reporting obligations will begin in September 2026, with full product security requirements following in December 2027. Non-compliance can result in fines up to €15 million or 2.5% of annual global turnover.

- Critical Entities Resilience Directive (CER): Complementing NIS2, the CER focuses on the physical and operational resilience of critical entities against all hazards, not just cyber threats. Entities identified as “critical” will face compliance obligations by mid-2026.

- Digital Services Act (DSA): This act modernizes rules for online intermediaries, imposing content moderation and reporting procedures on services that host user content.

United Kingdom Regulatory Developments

- Cyber Security and Resilience Bill: The UK is restructuring its cybersecurity regime with a bill that will expand scope to include data centers and managed service providers, introduce a new “critical suppliers” category, and establish a two-stage incident reporting model that differs from NIS2.

- Online Safety Act (OSA): This law takes an interventionist approach to user-generated content and child protection, applying to search engines and platforms that allow users to share content.

- Product Security and Telecommunications Infrastructure (PSTI) Act: This act targets the security of consumer-connected devices, banning universal default passwords and mandating clear vulnerability disclosure policies.

Canadian Privacy and AI Strategy

Canada is undertaking foundational reforms to its privacy and data landscape in 2026, driven by initiatives to modernize federal privacy law, establish data sovereignty, and implement a national AI strategy.

- Overhaul of Federal Privacy Law: A new federal private sector privacy statute is expected to be introduced in late 2025 or early 2026 to replace the Personal Information Protection and Electronic Documents Act (PIPEDA). The proposed law is expected to include severe penalties, with fines up to C$25 million or 5% of gross global revenue.

- Data Sovereignty: The federal government’s Digital Sovereignty Framework and Sovereign AI Compute Strategy signal a strong focus on maintaining domestic control over Canadian data and information systems to mitigate risks from foreign-based access.

- Federal AI Strategy: After the proposed Artificial Intelligence and Data Act (AIDA) died on the order paper, the federal government has shifted its approach. It now aims to regulate AI through a multi-faceted strategy involving privacy legislation, policy mechanisms, and strategic investment rather than comprehensive, standalone AI legislation.

- Open Banking Framework: Following the passage of the Consumer-Driven Banking Act (CDBA) in 2024, Canada is moving to implement its open banking framework. Complementary amendments to PIPEDA will establish an interoperable data mobility right, giving individuals the ability to direct organizations like banks to share their personal information with other authorized entities.

Global Regulatory Dynamics in the Cannabis Industry

The global cannabis industry is at a critical inflection point in 2026, marked by significant regulatory shifts that are creating both opportunities and immense compliance pressures. The sector’s increasing digitization and handling of sensitive data make it a prime target for cyberattacks and regulatory scrutiny.

United States: Rescheduling and Market Pressures

- Federal Rescheduling: The move to reclassify marijuana from Schedule I to Schedule III of the Controlled Substances Act represents a monumental policy shift. While not full legalization, it would remove the 280E tax penalty for plant-touching businesses going forward, materially improving cash flow. However, it will also heighten the compliance bar, increasing federal expectations for recordkeeping, auditability, chain-of-custody, and product controls.

- Hemp Market Contraction: Congress has moved to effectively ban the intoxicating hemp (e.g., delta-8) market with a container-level THC cap scheduled to take effect in 2026. This will impact revenue assumptions, inventory valuations, and risk exposure for operators in this segment.

- Cybersecurity and Data Privacy: As a data-rich and compliance-heavy sector, cannabis businesses are a prime target for cybercriminals. In 2025, 60% of businesses experienced at least one cyberattack. Dispensaries collect vast amounts of Personally Identifiable Information (PII) and Protected Health Information (PHI), triggering compliance obligations under state privacy laws and potentially HIPAA. Foundational requirements now include age-gated, logically related SMS consent for marketing.

International Regulatory Shifts

- Canada: In contrast to other trends, Canada provided significant regulatory relief to federal licence holders in 2025. Amendments to the Cannabis Regulations reduced burdens related to physical security, quality assurance personnel, packaging and labelling, record-keeping, and destruction processes.

- Germany: The German market is undergoing a significant reversal, pivoting toward “fully analogue care.” Proposed amendments to the Medical Cannabis Act seek to ban remote prescriptions via telemedicine and prohibit mail-order sales, fundamentally altering the business models of digital platforms. Germany is also pushing for GDPR reforms that would shift data protection liability from small medical practices to the manufacturers of standardized IT products under a “Privacy by Design” model.

- Thailand: Thailand is aggressively dismantling its post-decriminalization recreational market. New regulations in 2025 and 2026 re-establish a strict medical framework, confining sales to licensed medical facilities and pharmacies. This policy reversal is expected to cause the closure of thousands of general retail dispensaries that flourished after 2022.

- Colombia: The government is advancing a major reform of its Personal Data Protection Act (Statutory Act 1581) to align with GDPR standards, a critical move for facilitating cross-border data flows with European and North American partners.

Key Data Breach Statistics and Financial Impacts

Data from 2025 reveals a complex financial landscape for data breaches, with overall global costs decreasing slightly while U.S. costs and the impact of certain attack vectors continued to climb. The use of AI and automation has emerged as a critical factor in mitigating both the time and cost associated with a breach.

Headline Statistics

- Average Global Cost: The average cost of a data breach dropped 9% to $4.44 million in 2025 from its 2024 all-time high.

- Average U.S. Cost: The United States saw a 9% cost surge to $10.22 million, an all-time high for any region, driven by higher regulatory fines and detection costs.

- Breach Lifecycle: The mean time to identify and contain a breach fell to 241 days, a nine-year low. Lifecycles under 200 days were associated with cost savings of $1.14 million.

- Data Involved: Customer Personal Identifiable Information (PII) was involved in 53% of all breaches. Data theft was the second most common impact, occurring in 18% of incidents.

- Human Element: The human element was a factor in 60% of all breaches.

Cost Modifiers and Attack Vectors

The cost of a data breach is significantly influenced by the attack vector, the organization’s security maturity, and the technologies it employs.

Top Factors Increasing Breach Costs:

- Supply chain breach

- Security system complexity

- Shadow AI and adoption of AI tools

- Noncompliance with regulations

- Security skills shortage

Top Factors Decreasing Breach Costs:

- DevSecOps approach

- AI-driven and ML-driven insights

- Use of security analytics or SIEM

- Threat intelligence

- Employee training

How Different Attack Types Impact Your Bottom Line

The way attackers get in determines how much you’ll pay to get them out. Here’s what 2025 breach data reveals about costs and recovery times:

Malicious Insider Attacks: $4.92 million The most expensive breach type. When trusted employees turn malicious, detection takes an average of 260 days—over 8 months of undetected damage. Why so costly? Insiders know exactly where valuable data lives and how to cover their tracks.

Supply Chain Compromises: $4.91 million Nearly as expensive and even harder to detect. These breaches take 267 days on average to identify and contain—the longest of any attack vector. Third-party access creates blind spots that attackers exploit for months before discovery.

Ransomware Attacks: $5.08 million Actually the highest average cost in 2025, up 3% year-over-year. Modern ransomware combines encryption with data theft (double extortion), forcing organizations to pay both ransom demands and breach notification costs.

Phishing: $4.8 million Responsible for 16% of all breaches in 2025. While slightly less expensive on average, phishing remains the most common initial attack vector. One clicked link can grant attackers the same access as a legitimate user.

Accidental Insider Errors: $3.62 million The “least expensive” breach type, though still devastating. These incidents—misconfigured databases, misdirected emails, lost devices—take 213 days to identify and contain. The good news: they’re the fastest to resolve once detected.

The Pattern: Notice how insider threats (both malicious and accidental) appear twice on this list? That’s not a coincidence. When breaches originate from inside your organization, they’re harder to detect, more expensive to remediate, and take longer to contain than external attacks.

Emerging Threats and Mitigation Strategies

The threat landscape is rapidly evolving, with AI becoming a primary tool for both attackers and defenders. Insider threats and supply chain vulnerabilities remain critical and costly risks that require dedicated mitigation strategies.

The Impact of Artificial Intelligence

- AI as an Attack Tool: 1 in 6 breaches (16%) in 2025 involved AI-driven attacks. Attackers used AI most often for phishing (37%) and deepfake impersonation (35%). AI can generate a deceptive phishing email in 5 minutes, compared to an average of 16 hours for a human. The percentage of AI-assisted malicious emails doubled from 5% in 2024 to 10% in 2025.

- AI as a Defense Tool: Organizations with extensive use of security AI and automation identified and contained breaches 80 days faster and realized cost savings of nearly $1.9 million compared to organizations with no use. The use of AI and machine-learning insights was associated with 5% lower than average breach costs.

- AI Governance Gaps: A significant 97% of organizations that reported an AI-related breach lacked proper AI access controls.

Insider and Third-Party Risks

- Insider Threats: Malicious insiders cause the costliest breaches ($4.92M), while non-malicious insiders (negligent or outsmarted) account for 75% of all insider incidents. The average annual cost of insider-led incidents reached $17.4 million in 2025.

- Third-Party & Supply Chain Risk: Breaches originating from a supply chain compromise were the second most prevalent and second costliest attack vector ($4.91M) and took the longest to resolve (267 days). A major concern is that organizations assess only 40% of their vendors on average, primarily due to understaffed third-party risk management programs.

[Vibe Hacking Security Assessment | Security for AI-Generated CodeIdentify and fix security vulnerabilities in AI-generated code with our comprehensive assessment tool and tailored AI prompts.